The #1 Financial Mistake Small Business Owners Make (And How to Fix It)

A San Francisco Bay Area CPA's answer to the question every business owner needs to hear.

The #1 Financial Mistake Small Business Owners Make (And How to Fix It)

The most common financial mistake small business owners make is running their company off bank balance instead of off real financial statements. Bank balance hides debt, accounts payable, and upcoming obligations, so spending decisions get made on a false picture. The fix is simple to describe and brutally hard to skip: review your financial statements every single month. Five reports do the heavy lifting. Profit and Loss, Balance Sheet, Statement of Cash Flows, Expenses by Vendor, and Sales by Customer.

Read in that order, once a month, and your decisions get smarter immediately. Most owners do this annually or quarterly and pay for it the rest of the year. Asnani CPA Tax & Accounting in the San Francisco Bay Area handles this for clients through our outsourced accounting service, so the monthly review actually happens.

The Mistake: Running Your Business Off Your Bank Balance

Ask a hundred small business owners how they decide whether to spend money this week, and ninety of them will tell you the same thing. They check the bank account.

That's the mistake. And it's the most common financial mistake we see at Asnani CPA Tax & Accounting, full stop.

Here is the problem with bank balance thinking. The number sitting in your checking account is not your money. Part of it belongs to your credit card. Part belongs to next month's payroll. Part belongs to the IRS in quarterly estimates you have not paid yet. Part belongs to a vendor whose invoice is due in eleven days. Bank balance shows you a snapshot of cash on hand. It does not show you what that cash is already promised to.

When you make spending decisions on bank balance alone, you are running a "how much can we spend today" operation instead of a business. You feel rich on the 5th of the month and broke on the 25th. You stop knowing whether you are actually profitable. Worst of all, you cannot tell if a slow month is a bad month or a great month with delayed invoicing.

The cost is not just stress. The cost is bad decisions, made confidently, repeated for years.

What I Wish Every Business Owner Would Do Differently

Review your financial statements once a month. Not annually. Not quarterly. Monthly.

That is the single change that separates business owners who scale from business owners who tread water.

Monthly reviews force you to look at the actual numbers before they get old enough to lie to you. Annual reviews are autopsies. Quarterly reviews are check-ups. Monthly reviews are how you actually run the business.

I know financial statements feel intimidating. They feel like a foreign language designed by accountants to make business owners feel stupid. They are not. There are five reports that matter, each one answers one simple question, and once you know which question each report answers, the fear disappears.

The 5 Reports Every Small Business Owner Should Review Monthly

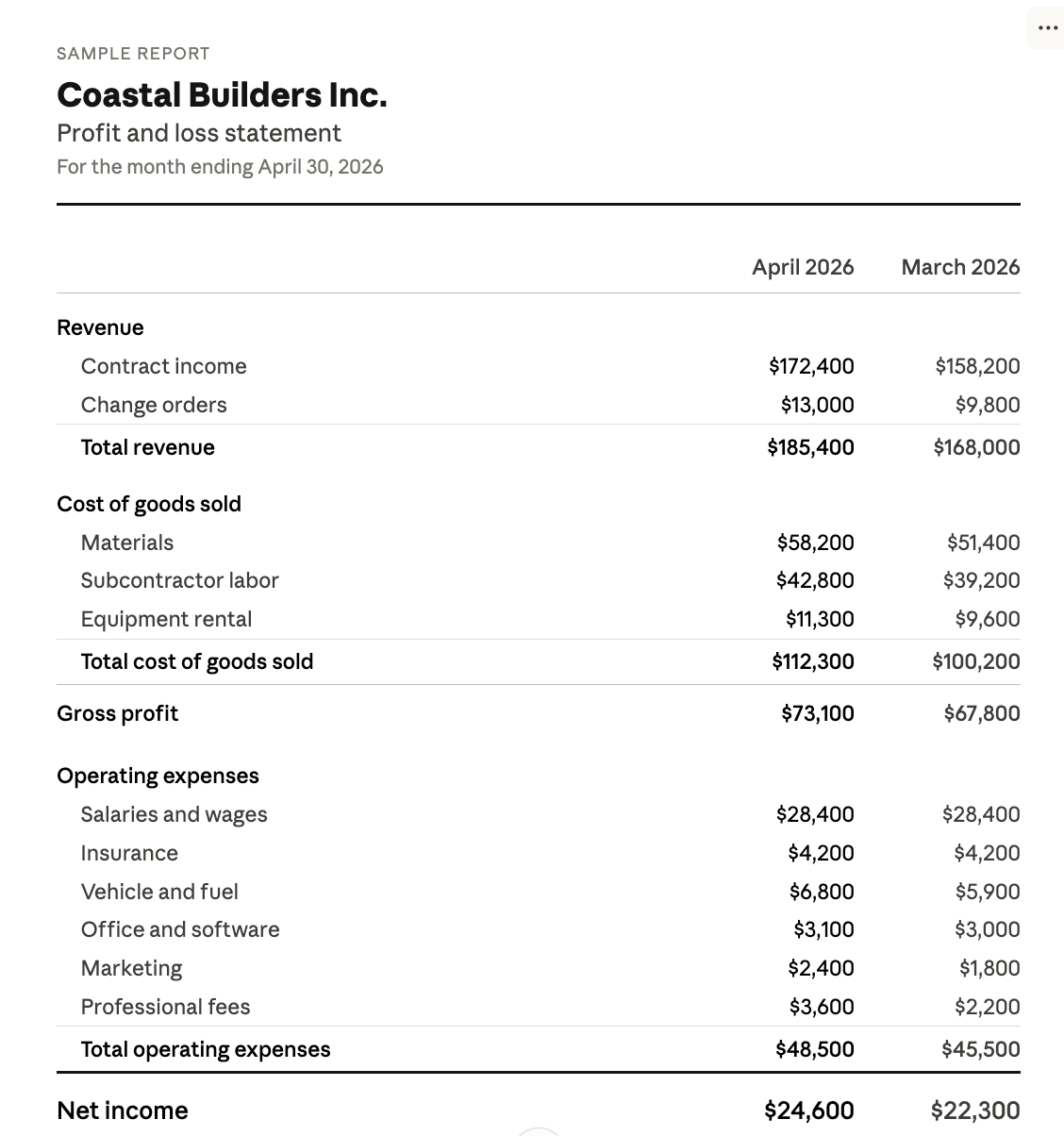

1. Profit and Loss Statement (P&L)

The question it answers: How much did we make, and how much did we spend?

The P&L shows revenue at the top, expenses below, and profit at the bottom. It tells you whether the business itself is making money, separate from any cash timing quirks. A profitable month with bad cash flow is a different problem from an unprofitable month with great cash flow. Both look bad in the bank account. Only the P&L tells you which one you have.

Look at gross profit, operating expenses, and net profit. Compare this month to last month, and this month to the same month last year. Patterns show up fast.

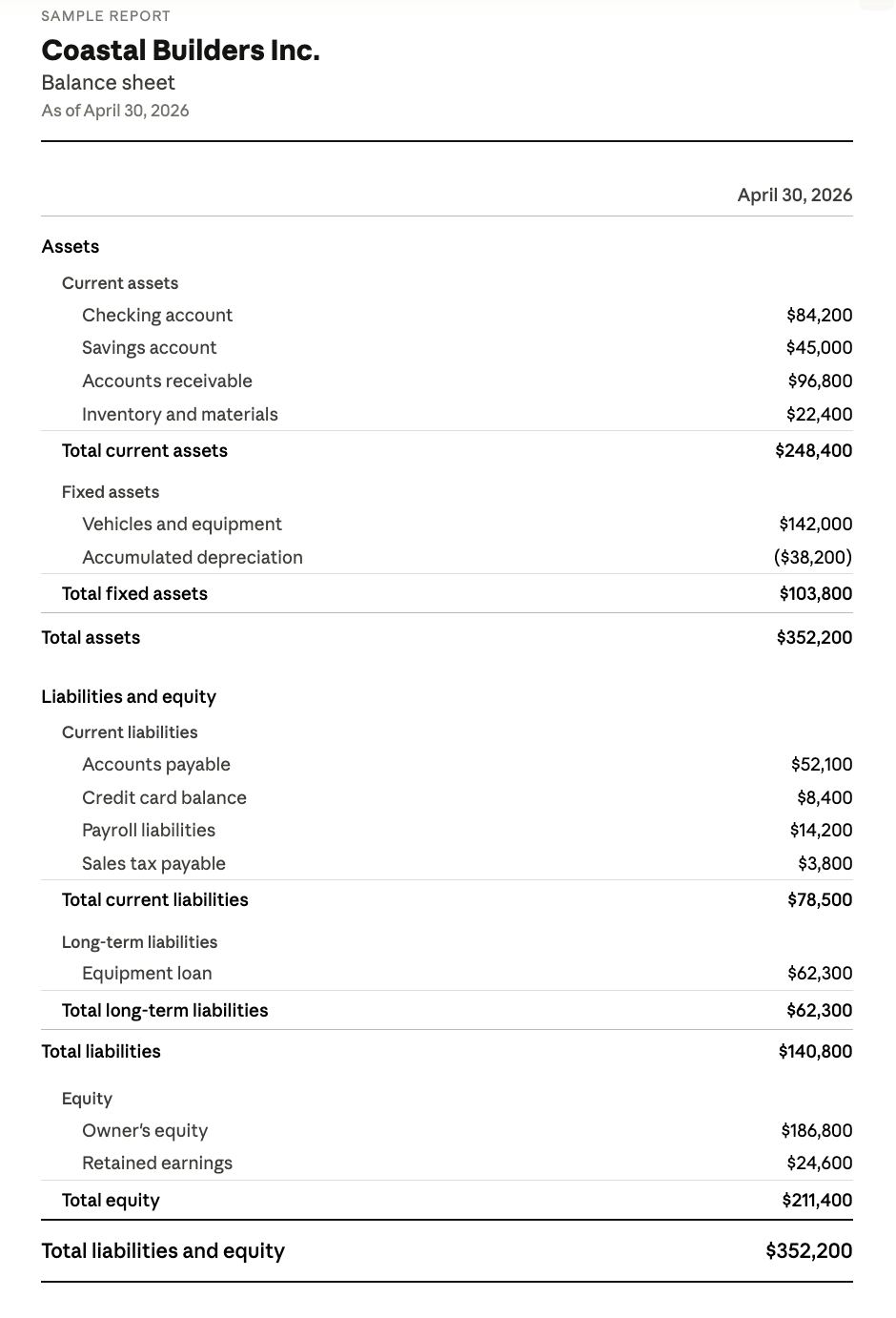

2. Balance Sheet

The question it answers: How much do we actually have? Are we in debt?

The Balance Sheet is the report bank balance thinking ignores. It shows assets (what you own), liabilities (what you owe), and equity (what's left). A healthy balance sheet is not about having a lot of cash. It's about having more assets than liabilities, and having the right kind of liabilities.

Three things to watch every month. Accounts payable (what you owe vendors). Accounts receivable (what customers owe you). Total liabilities versus total assets. If accounts payable is growing faster than accounts receivable, you are sliding into trouble whether the bank account knows it or not.

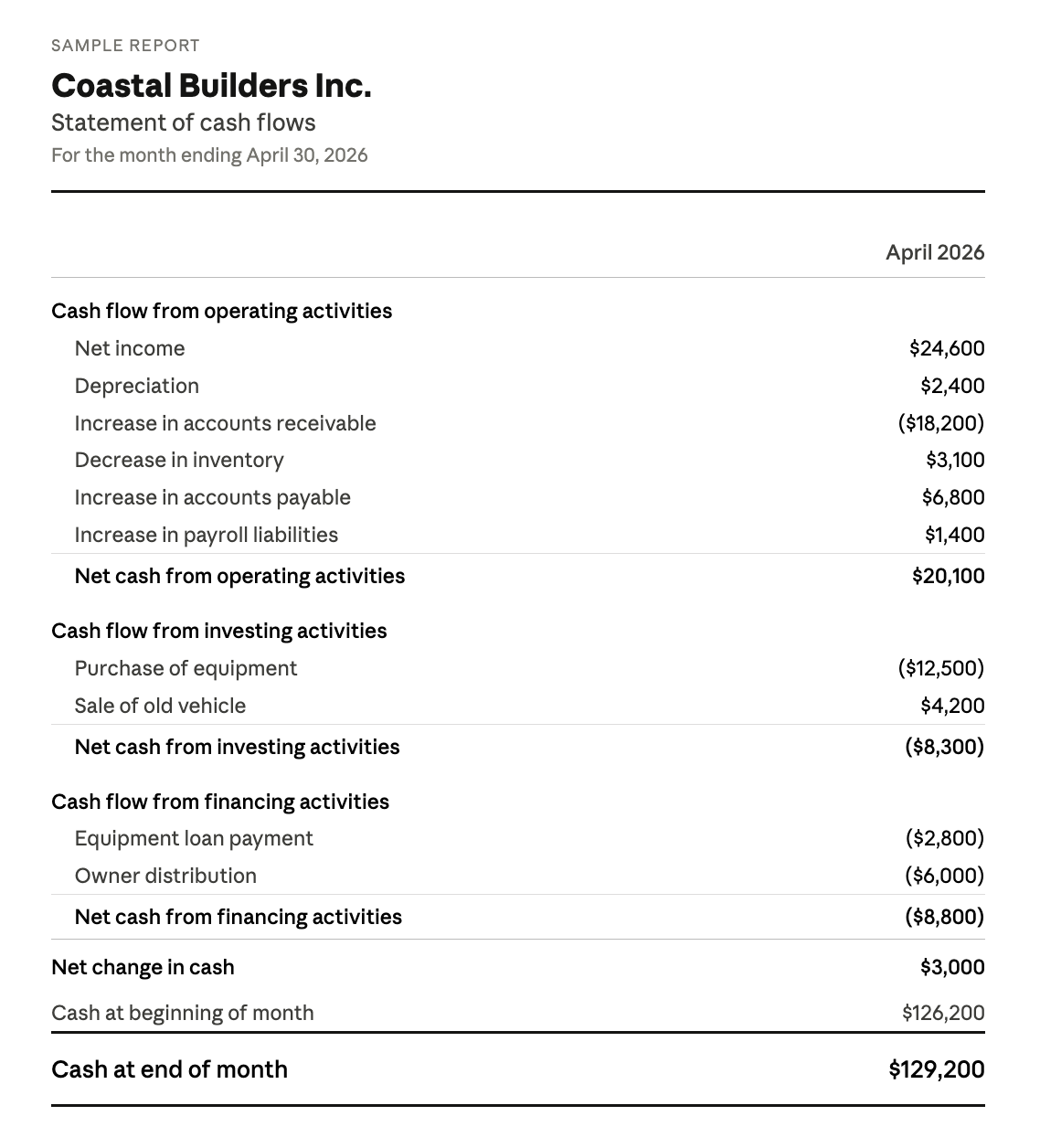

3. Statement of Cash Flows

The question it answers: What did my money actually do? Did I see the cash from my profit, or did it go to paying debt?

This is the bridge between the P&L and the bank account. Cash flow gets divided into three buckets. Operations (cash from running the business). Investing (cash spent on equipment, property, or other long-term assets). Financing (cash borrowed or paid back on loans).

If your P&L shows a profitable month but cash flow from operations is negative, your customers are paying you slowly. If financing activities are propping up the business, you are borrowing to stay alive. The Statement of Cash Flows surfaces both problems in five minutes.

The IRS has a clean explainer on understanding cash flow for small businesses that pairs well with this report.

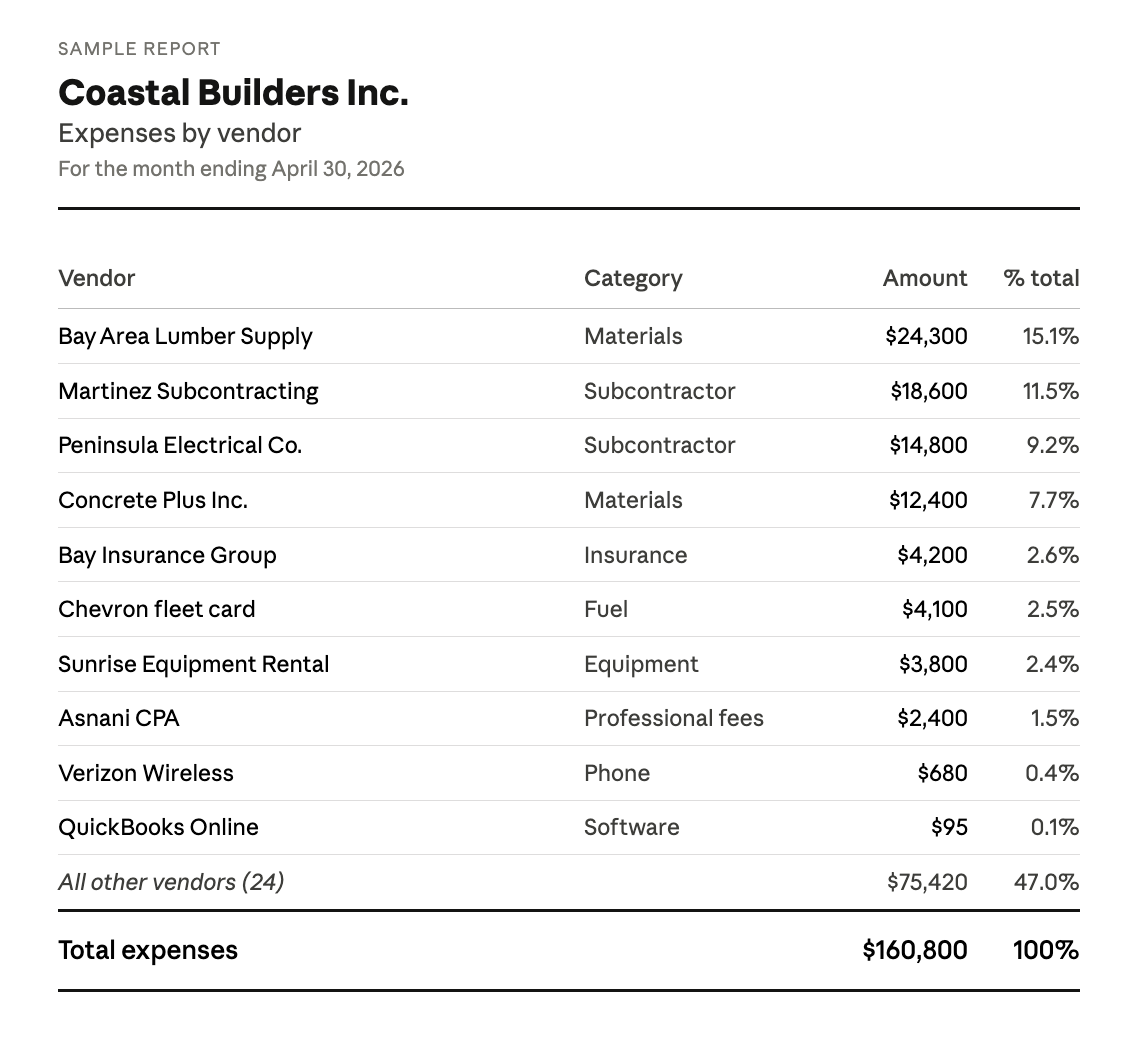

4. Expenses by Vendor

The question it answers: Who did I pay?

This report ranks every vendor you paid this month, from largest to smallest. It is the single most useful report for finding wasted money. Software subscriptions you forgot about. Vendor creep where small invoices have quietly tripled. Suppliers you are over-relying on. Recurring charges from services you no longer use.

Spend ten minutes on this report each month and you will find money. Most owners do.

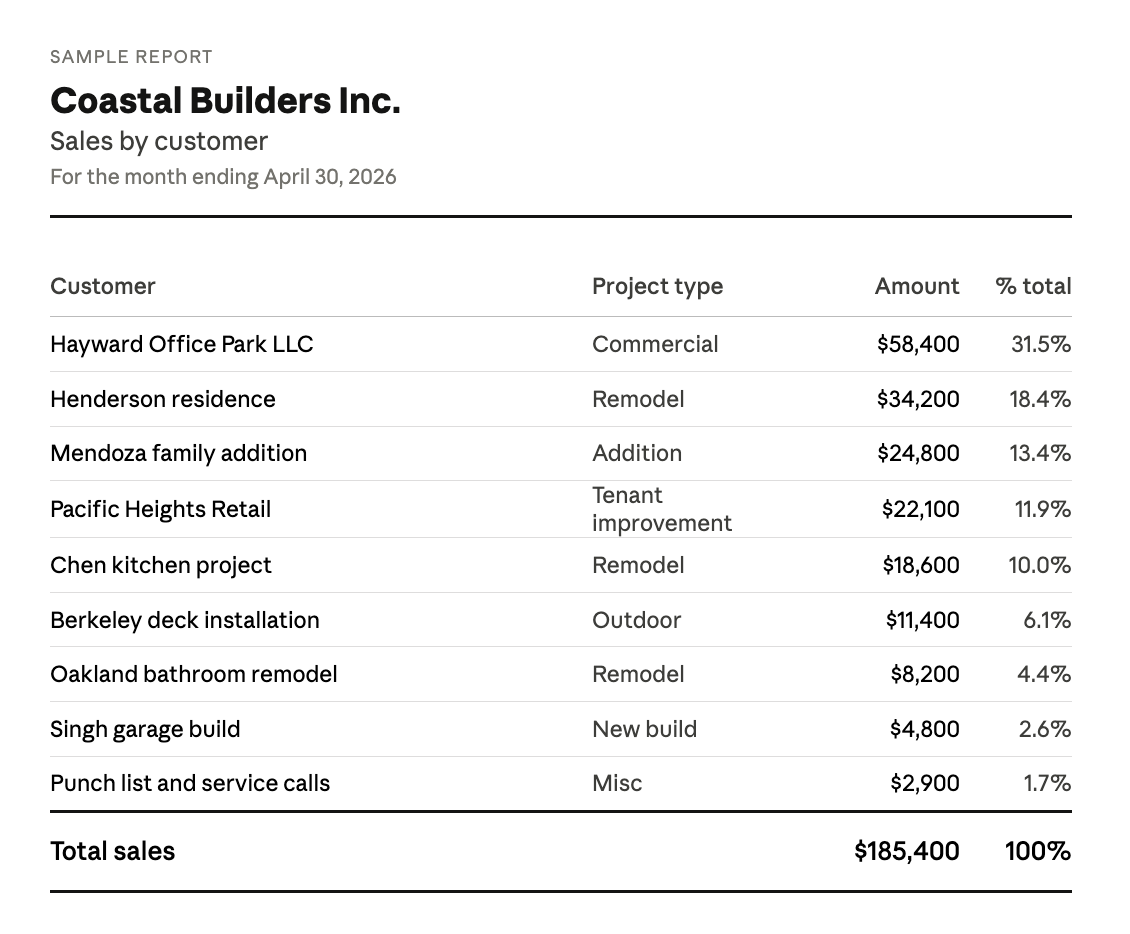

5. Sales by Customer

The question it answers: Who paid me?

The reverse of Expenses by Vendor. Rank every customer by what they paid, largest to smallest. You will learn three things fast. Who your real top customers are (often not who you think). How concentrated your revenue is (anyone over 20% of revenue is a risk). Which customers have stopped buying without you noticing.

Customer concentration risk kills small businesses. If one customer leaves and takes 35% of revenue with them, your business goes from profitable to dead overnight. The Sales by Customer report is how you see that risk before it happens.

Why Monthly, Not Quarterly or Annually

I get asked this constantly. Why monthly?

Three reasons.

- Decisions don't wait for quarters. You make hiring, spending, pricing, and inventory decisions every week. If your data is sixty days old, your decisions are sixty days late.

- Monthly catches problems while they are still small. A vendor charging you double in January is a $200 problem in February. Caught in October, it's a $2,000 problem and ten months of cleanup.

- Annual reviews teach you nothing useful in time. By the time your CPA shows you the year-end financials, the year is over. You cannot fix what is already done. You can only avoid repeating it.

Quarterly is better than annually. Monthly is better than quarterly. There is no version of this where less frequent wins.

Why Most Business Owners Don't Do This

If monthly financial reviews are so important, why do almost no business owners do them?

Three reasons, in our experience working with small businesses across the San Francisco Bay Area.

- The books are never caught up. You cannot review what does not exist. Most small business bookkeeping runs three to six months behind. Some owners have never seen current financials in their entire business career.

- The chart of accounts is generic. A default QuickBooks setup gives you generic categories that hide what is actually happening. A properly built chart of accounts shows you job-level profitability, customer-level profitability, and category-level spending in a way you can actually use. Most are not built that way.

- No one walks them through it. Reading a balance sheet for the first time is hard. Reading one once a month, with someone who can explain what changed and what it means, is easy. Most owners have never had the second experience, so they avoid the first.

How Asnani CPA Solves the Monthly Review Problem

Standalone bookkeepers reconcile transactions and hand you a stack of reports. That solves the data problem. It does not solve the interpretation problem, and it definitely does not solve the tax problem.

Our model at Asnani CPA Tax & Accounting is built differently. We call it outsourced accounting, and it bundles four things that normally sit with four different vendors.

- Monthly bookkeeping that actually finishes monthly. Our bookkeeping service closes your books every month, on time, with a chart of accounts built for your specific business. Not a generic QuickBooks template. We rebuild it so the reports tell you what you need to know.

- Payroll integrated with everything else. Most business owners pay separately for payroll, then pay again to have someone reconcile it. Our payroll service sits inside the same team that does your books, so payroll posts correctly to financials the first time.

- Tax planning that uses the monthly data. This is the part most accountants skip. When we close your books each month, we are also looking for tax reduction opportunities in real time. S-Corp salary decisions, equipment depreciation timing, retirement contributions, and quarterly estimate payments all benefit from monthly visibility. Reactive tax accountants only see this data once a year, after you can no longer act on it. Our business tax return and planning service is built on the books we already maintain.

- CFO-level guidance built into the relationship. When we send monthly financials, we are not just sending reports. We are flagging customer concentration, vendor creep, margin compression, and cash flow trends. Pre-revenue tech founders get the same treatment through our accounting for startups practice, where GAAP compliance and burn rate tracking matter from day one.

Why Bay Area Business Owners Choose Asnani CPA

We are based in the San Francisco Bay Area and exclusively serve businesses. Not "exclusively" as a marketing phrase. We literally do not take personal-only tax clients, because we have built the team and systems around small business owners, freelancers, 1099 earners, and growing companies.

Our clients run general contracting businesses, landscaping companies, digital agencies, professional services firms, and tech startups across San Francisco, Oakland, San Jose, Mountain View, Berkeley, San Mateo, and Hayward. We are not "too busy" to provide proactive tax planning, because we built the model around having the time to do it. The Small Business Administration's guide to financial management is a fine place to start, but the difference between reading about monthly financial review and actually having one happen is who is doing the work each month.

If you want to know exactly what is in your business every month, and you want a tax plan built on real numbers instead of last year's tax return, we should talk. We start every relationship with a no-cost Tax and Accounting Analysis.

Reach out to Asnani CPA and schedule your free Tax and Accounting Analysis.